Gas Supply & Demand Study

Last week the Gas Industry Company issued a New Zealand gas supply and demand study. It makes for pretty sobering reading as this newsletter has previously predicted. Let's have a closer look.

The Gas Industry Company (GIC) works alongside the industry and the government in a type of soft regulatory capacity. They interface with the industry on supply, looking at demand trends and then recommending policy positions to the government to best manage this critical resource. They also keep a wealth of data that is interesting and worth a visit to their website Gas Industry Company.

The GIC have recently collaborated with Ernst Young (EY) to produce the “Gas supply and demand study 2023”. As predicted the picture is grim and we are on the cusp of significant issues with predicted demand, despite falling, outstripping supply as early as 2025.

The full report can be found here Gas supply and demand.

This supply issue will of course come as no surprise to readers of this newsletter as I predicted this issue would arise in my first post in August of this year “Cooking with the gas, or maybe not?”.

Cooking with the gas! or maybe not?

New Zealand’s introduction to gas as an energy source came with the 1959 discovery of the Kapuni gas field in Taranaki followed by the introduction of a gas distribution network in 1970. The introduction of a domestic gas supply in New Zealand was the fertile ground upon which industry grew. Following on from Kapuni was the Maui offshore gas field ten y…

Let’s dive into the report and see what they have to say. It’s quite a chunky document at 155 pages so I’ll distil it down to the key issues an provide some commentary.

Firstly, it’s important to understand the terminology and a few assumptions that have been used in the analysis. This report uses the 2P gas reserve profile as the basis for the analysis.

For clarity:

1P = Proven

2P = Proven + Probable.

“P” reserves must be possible to recover using current technologies in such a way that they are profitable.

The 1P gas reserves as of January 2023 were 1030 PJ.

The 2P gas reserves as of January 2023 were 1651 PJ.

The report also relies heavily of 2C “contingent” reserves. Contingent reserves are reserves that are potentially recoverable from known formations but not currently considered commercially viable.

I estimate that we will use somewhere between 160-180 PJ of gas as a nation in 2023.

I also predict that there will be reserve write downs in the next reporting period. This means that the remaining gas reserves reported in January 2024 will be less than the 2023 figure minus the 2023 consumption. Why do I predict this? Because the bigger fields are aquifer driven, difficult to evaluate and prone to watering out. Write downs have been increasingly common in recent reserve profiles.

For this report to be accurate we would need to be able to recover all of the “probable” 2P reserves. This is overly optimistic assumption as these reserves are scattered across the various fields and much of it un-economic to recover. The following table shows the difference between the 1P & 2P reserves for the various fields.

As you can see most of these 2P increments are too small to be economically viable when the cost of drilling is considered. It is likely that the only viable onshore “probable” reserves to recover for the 2P profile are at Turangi, Ohanga, Onearo, Urenui and Mangahewa. Assuming a multiple well campaign exceeded our wildest expectations in terms of success these fields would add around 273PJ (or approx 1.5 years) of reserves.

As there is very little drilling going on current and little if any planned for 2024, the only 2P gas reserves that may be added this year are from Kupe, which I would estimate at around 30PJ based on the table above.

Because this report uses the 2P and because I expect more write downs when the 2024 MBIE reserves are published next year, I feel that this report is weighted on the optimistic side. It also has quite an optimistic view on the feasibility of hydrogen and biogas (which incidentally is just methane like the non-biogas but that’s a post for another day).

The report structure:

The report looks at four scenarios. I am pleased to see that one of them is “Methanex Exits Early”. This considers Methanex leaving the country when their current gas supply contract finishes in 2029. This is significant because Methanex uses around 50% of the gas produced, and in doing so have underwritten a lot of exploration in the past, in order to secure long term gas supply agreements.

Is it a realistic scenario that Methanex would exit New Zealand? Yes, it is possible. They have a large plant that needs regular shutdowns (turn arounds) for inspection and recertification. This work represents a huge cost. This expenditure needs to be underpinned by security of supply to recover the investment made in the turn around.

The other three scenarios are all with Methanex remaining in operation. They are:

Industry Focus:

Essentially the current situation where petrochemical production (methanol and ammonia urea) consumes the bulk of the natural gas supply.

Elevate Electricity:

Considers a future where the electricity sector is more heavily reliant on gas for its own security of supply for longer. This is highly likely. However, generation capacity may be more of a limiting factor than gas supply as noted in an earlier post called Energy & Economy Assuming we have sufficient gas peaker plant generation capacity we are likely to need gas to back up an ever-increasing penetration of intermittent “renewables” into the electricity generation mix.

Supply Headwinds:

Looks at the current supply being constrained or dropping further. They frame it as demand dropping due to lack of supply. This is an interesting framing and would be better described as “economic activity is not sustainable due to a lack of gas supply”.

Report analysis:

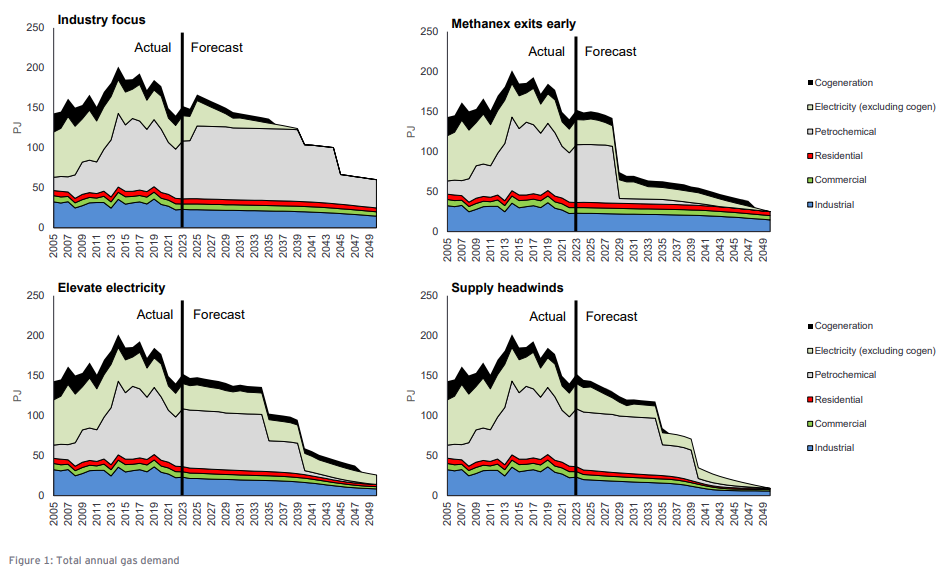

Demand:

Firstly the report looks at the demand forecast of the four scenarios.

These clearly show how big the impact of Methanex (the grey segment) is on the demand forecast. The other three demand scenarios are very similar with the only real difference being a longer tail within the industry focus scenario.

Buried in the text you will find that the length of the tails in each scenario is actually governed by the date that Methanex operates out to. This makes sense, as I would expect the other industrial users to continue on a similar demand profile due to a lack of viable alternatives and increased electrification will increase gas use due to the intermittent nature of the technologies proposed needing to be backed up.

One of the common assumptions I hear is that if Methanex exists that there will be more gas for the remaining consumers. This is an overly simplistic view as the whole market dynamics would change. The size of the NZ gas market would halve overnight, and we would immediately be in an oversupply scenario. This would have significant downward pressure on wholesale gas prices. This sounds good but the full implications are that the highest cost production would no longer be economically viable. We would see the high operating cost offshore fields shut in and move to a decommissioning phase. This would strand the remaining reserves in these fields diminishing the total recoverable reserves. The EY report does not consider this outcome in their analysis.

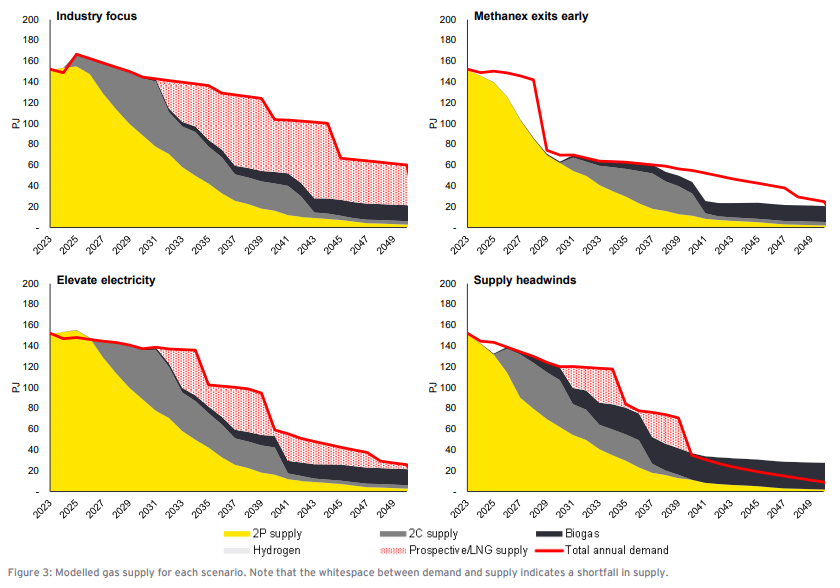

Supply:

This chart maps the supply profile from the various fields. Remember this is a 2P forecast and predicts that the “probable” piece of the reserves will all be recovered. Another key take out is the dark grey wedge on the right-hand side, this is 2C reserves. The “C” in 2C stands of “contingent”. 2C resources are the best estimate of contingent resources, which are amounts of gas that are potentially recoverable from known accumulations but are not yet considered commercially viable. The likelihood that these will be recovered without a big consumer to underwrite the associated drilling campaigns, which are not guaranteed to deliver, is extremely low. As such I believe this supply forecast is optimistic even in the short term.

Supply vs Demand:

This is where the rubber hits the road and things get interesting.

Focus on the red line and the yellow wedges. The yellow wedge is 2P supply, gas that we think we probably have available. The red line is the demand forecast.

In all scenarios the red line and yellow wedge diverge very quickly. 2025 in the worst case and 2027 in the best case.

The big grey wedge to save the day is “contingent” reserves that will suddenly appear from 2025. Given that it takes a minimum of 18 month to even get a consent to go drilling the chances that this will eventuate is zero.

We will very quickly see demand outstrip supply, and no hydrogen will not save the day despite what the media breathlessly tell you. Hydrogen has a troubled relationship with thermodynamics and molecular physics making it both expensive and problematic.

Even if the “probable” or “contingent” reserves were available the lead time to recover them is just too long to avoid a supply deficit.

Our government departments have not been focused on energy security and have instead been romanticizing over “renewable” technologies that in most cases are yet to be, or unlikely to ever be, commercially viable and scalable.

We have been caught with our pants around our ankles.

What does it all mean?

I don’t really know how this will playout to be honest. What I do know is that there are no good outcomes and only varying degrees of bad.

I would expect it to play out something like this.

In the short-term industrial petrochemical production will be curtailed to meet the requirements of other industries. This will primarily effect Methanex. In the short term it may be more profitable for them to on sell their contracted gas than it is to produce methanol. However, this will ultimately lead them to the conclusion to exit as the gas they need for future production and to support investment in their plant is not available in sufficient volumes.

This will in turn have a flow on effect to the offshore fields which will likely be decommissioned earlier than expected and as a result there will be a significant reserve write down.

As the market contracts prices will initially drop then rise significantly as the market becomes supply constrained again. The dairy industry in particular is vulnerable as Fonterra uses approx. 7PJ of gas to run their factories and dairy farmers use a lot of urea as fertilizer produced from gas, by Balance, to support their production.

Electricity markets will also be affected initially by cheap gas from the oversupply stalling investment in new generation capacity, then by expensive and scarce gas causing large price spikes in the wholesale market.

There is of course a lot of nuance due to commercial arrangements etc. But this is a rough outline of what could eventuate.

New Zealand is de-industrializing already and this trend is about accelerate rapidly. We are following a similar trajectory to German due to our failure to prioritize cheap, abundant and secure energy. Energy and GPD have a 1:1 relationship. Energy scarcity equals recession or depression. Our standards of living will follow the same trajectory.

I am sorry for the grim message but there is no way to sugar coat this. I had sincerely hoped that my earlier projections would be proven wrong, but this report suggests I am on the right track.

I don’t know what the short-term answer is either, particularly when I consider the mountain of Govt. debit we are saddled with and the new fiscal landmines that are being discovered daily thanks to Grant Robinson. This financial position limits our ability to respond at scale.

If I were Simeon Brown, as the incoming energy minister, I would be immediately meeting with the field operators to give certainty and fast track drilling activities to shore up the short-term supply issues. I would also meet with Methanex to ensure the market dynamic issues can be avoided. I would abandon any fairytale notions that I had about offshore wind saving the day and immediately send a delegation to Korea to look into nuclear generation options for New Zealand’s longer term electricity requirements. As unpalatable as it would be cost wise, I would also immediately put plans in motion to have LNG importation infrastructure in place as a contingency plan.

Hold on tight folks it’s going to be a bumpy ride!

Do you think this could get us to finally discussing nuclear? (I'm looking for silver linings)

Sad to read but so accurate 😳