Free energy?

It's the infrastructure my friends.

Much is made of renewables being “free” in the media and marketing we are bombarded with on an almost daily basis. However, if this is the case, then why are they consistently so expensive?

The truth, as always, is somewhat more nuanced.

Until the Government finds a way to tax us for the solar energy flows from the sun, all energy is in essence free.

It’s the cost of the infrastructure to harness an energy source, and convert it to a useful form, that ultimately sets the price of energy.

The cost of the infrastructure is primarily related to two fundamental qualities of any energy source, energy density and intermittency.

Low energy density = high resource intensity (lots of infrastructure).

Intermittency = the need for redundancy and/or storage (lots more infrastructure).

This is why intermittent renewables, such and wind and solar, inevitably become increasingly expensive as they occupy a larger percentages of generation capacity in any national grid.

Offshore Wind Economics

I was prompted to write this post while perusing the NZ Govt. MBIE consultation paper on “Developing a Regulatory Framework for Offshore Renewable Energy: Second Discussion Document August 2023”.

Here a few extracts that piqued my interest…

Chapter 6: Economics of the Regime.

Internationally there are a range of economic models associated with offshore renewable energy. Many overseas regimes have one or both of the following features:

A support mechanism – a payment flow from government to the offshore renewable energy project. This can lower costs compared to alternative forms of energy, or provide revenue certainty to enable the project to access cheaper financing.

A revenue gathering mechanism – a payment flow from the project to government. This usually enables the taxpayer to benefit from the development of the offshore renewable energy sector.

Before you get too excited about the “revenue gathering mechanism” the consultation paper quickly dampens your enthusiasm with this humorously ironic sentence.

The government might gather revenue from a project, but, as this will increase project costs, it may also increase the likelihood that government would need to use this revenue to provide a revenue support mechanism.

So, it’s a zero-sum money go round?

Well not quite. Based on international experience I can confidently speculate that these revenue flows will be largely one way. From the Govt. taxpayer to the project.

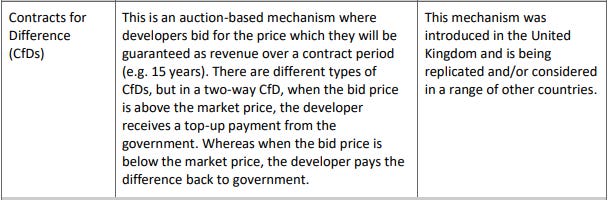

The paper homes in pretty quickly on a preferred “dual feature” mechanism known as CfDs (Contracts for Difference).

This mechanism is also commonly known as “strike price” in the UK. How this works in practice is that a developer essentially bids for a project based on a strike price, which is the price paid for each MWh of electricity generated, regardless of the market price at the time.

If the market price is below the strike price the developer gets a top up from the taxpayer for the difference. If the market price is above the strike price the developer reimburses the taxpayer for the difference.

This is what the folks at MBIE had to say about this preferred mechanism.

Looking at international examples it is evident that the design of these mechanisms has evolved over time, reflecting increasing technological maturity and falling project costs. More specifically:

where a subsidy is offered, the level of subsidy has typically fallen

there is an increasing trend toward revenue stabilisation mechanisms rather than subsidy mechanisms (i.e. mechanisms that provide revenue certainty, but do not necessarily result in a subsidy (e.g. a two-way CfD))

the first projects without any government support are starting to come online in Europe.

Unfortunately for MBIE these predictions haven’t aged well at all. A few short months after their consultation paper was issued the UK Govt. did not receive any bids at the most recent auction. As a result, they have had to raise the strike price by 66% in an attempt incentivize developers. Furthermore, projects based on earlier bids are being cancelled. S&P Global summarize the situation in this article.

The UK government has increased the maximum price for offshore wind in its next renewables auction by 66% to combat rising project costs, the Department for Energy Security and Net-Zero said Nov. 16.

The maximum strike price will rise from £44/MWh to £73/MWh for fixed-bottom offshore wind in 2024's contracts for difference (CFD) auction after this year's bidding process failed to award a single offshore wind contract because of the low ceiling price.

The move comes as developers continue to face inflated costs and rising interest rates, with Swedish utility Vattenfall AB this year suspending development of its 1.4-GW Norfolk Boreas offshore wind farm. The project won a contract in 2019's CFD auction at £37.35/MWh.

All CFD prices are given in real 2012 currency, with offshore wind's new strike price equating to about £100/MWh in nominal terms, according to analysts at RBC Capital Markets.

The new bid ceiling for Allocation Round 6 will help ensure projects are economically viable and shore up new capacity as the UK pursues 50 GW of offshore wind by 2030, the government said.

The question that must be asked is economic for who? Surely not the consumers or taxpayers, who are one in the same.

This is the economics of intermittency.

But it does not stop there. The people of the UK also have to contend with “constraint payments”.

This is how the UK Electricity Service Operator ESO describe constraint payments.

When there are physical constraints on the network (ie the network cannot physically transfer the power from one region to another), we ask generators to reduce their output to maintain system stability and manage the flows on the network.

Generators are then compensated via a constraint payment. The alternative is building more infrastructure at a significant cost, meaning higher bills for consumers.

This is what constraint payments look like in practice.

Energy bill payers were forced to fork out a huge £205m to wind farm giants in Scotland so that they turned off their turbines amid a windy and wild year for weather. It means that 2024 could mean a record amount of cash being supplied to renewable energy operators to stop producing electricity.

MBIE do not mention a constraint payment mechanism in their consultation paper. However, given the size of NZ’s grid, constrains with the HVDC inter island link, and the bulk of NZ’s hydro being in the South Island limiting ability to buffer, it is inevitable that this will be an issue when you have 1 - 2 GW of offshore wind generation swinging in and out of a 5 - 7 GW grid due to the vagaries of the weather.

On top of constraint payments, we also need a commercial mechanism to include the cost of firming capacity which is redundancy in either storage or other forms of generation required to keep the grid alive on those cold frosty windless days.

So, how empirically has the price of electricity trended in the UK since the first “free energy” offshore wind farm was built in 2000?

It would be disingenuous of me to suggest that all this increase can be attributed directly to offshore wind. It’s also attributable to the rising costs of other fuel sources, geo-politics and other factors.

The key takes away from this however, is that the promised cheap power from an energy transition has not eventuated.

This is again the economics of intermittency, multiplied by low energy density (high capital cost).

As the saying goes… there’s no free lunch.